http://www.imf.org/external/pubs/ft/wp/2010/wp10268.pdf

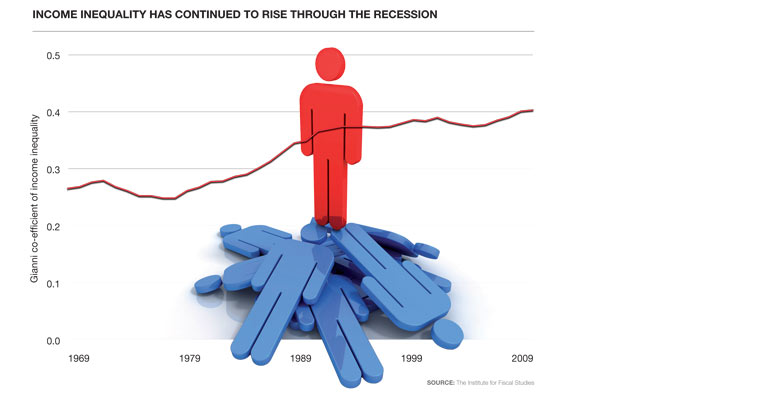

In their paper about the relationship between inequality and crises, the economists Michael Kumhof and Romain Rancière try to go beyond the simplistic notion that economic crises are merely a result of personal incompetence plus greed plus bad loans. They look at one of the less researched aspects of the US market, which otherwise is closely related to bank failures - namely, the level of financial disparity between the various segments of society. They analyzed the data for the last century, particularly the periods of the greatest crises, 1929 and 2008. In both cases they've found that the gap between wealthy and poor had opened beyond a certain critical level. Their conclusion: there's a pattern showing that whenever the top 5% possess 34% of the total wealth or more, the level of private loans would tend to double within a short period of time.

Their logic is simple. In order to be able to consume goods and services, people with lesser financial capabilities are compelled to take loans which they eventually turn out incapable of paying back. Meanwhile, the wealth of the top segment swells to such proportions that they begin investing considerable amounts in supposedly highly profitable loan deals. Taking extra risks, hoping for easy gains - because they can afford it. Eventually when the loans stop being served, the whole system collapses.

The solution the two authors are proposing is that workers in general should reach salary levels at least as much as to not be compelled to support their living standard through loans. Which, I think, neglects the counter-argument - that people should try to live within their means in the first place - a notion that has become so alien to Western lifestyle. There's also the objection that, as household income increases, so do the needs and aspirations of the household members, and the living standard that's being pursued. I.e. "money is never enough". On the other hand, the authors counter this argument by looking at the data and demonstrating that the general consumption among the wealthiest segments tends to increase at a much slower rate as they become richer; that extra money being invested in speculative deals for the most part, for the sake of easy, but risky profit. In other words, beyond a certain level of wealth, the wealthy stop creating more jobs and doing a real contribution to the economy and start hoarding and/or outsourcing their capital, and pump up artificial balloons, relying that they'd play smartly and pull out, and avoid being affected by the inevitable bust. And all of that distorts the whole credit climate, and ultimately the ones paying the bill for most of the damage control are again the lower segments.

In their paper about the relationship between inequality and crises, the economists Michael Kumhof and Romain Rancière try to go beyond the simplistic notion that economic crises are merely a result of personal incompetence plus greed plus bad loans. They look at one of the less researched aspects of the US market, which otherwise is closely related to bank failures - namely, the level of financial disparity between the various segments of society. They analyzed the data for the last century, particularly the periods of the greatest crises, 1929 and 2008. In both cases they've found that the gap between wealthy and poor had opened beyond a certain critical level. Their conclusion: there's a pattern showing that whenever the top 5% possess 34% of the total wealth or more, the level of private loans would tend to double within a short period of time.

Their logic is simple. In order to be able to consume goods and services, people with lesser financial capabilities are compelled to take loans which they eventually turn out incapable of paying back. Meanwhile, the wealth of the top segment swells to such proportions that they begin investing considerable amounts in supposedly highly profitable loan deals. Taking extra risks, hoping for easy gains - because they can afford it. Eventually when the loans stop being served, the whole system collapses.

The solution the two authors are proposing is that workers in general should reach salary levels at least as much as to not be compelled to support their living standard through loans. Which, I think, neglects the counter-argument - that people should try to live within their means in the first place - a notion that has become so alien to Western lifestyle. There's also the objection that, as household income increases, so do the needs and aspirations of the household members, and the living standard that's being pursued. I.e. "money is never enough". On the other hand, the authors counter this argument by looking at the data and demonstrating that the general consumption among the wealthiest segments tends to increase at a much slower rate as they become richer; that extra money being invested in speculative deals for the most part, for the sake of easy, but risky profit. In other words, beyond a certain level of wealth, the wealthy stop creating more jobs and doing a real contribution to the economy and start hoarding and/or outsourcing their capital, and pump up artificial balloons, relying that they'd play smartly and pull out, and avoid being affected by the inevitable bust. And all of that distorts the whole credit climate, and ultimately the ones paying the bill for most of the damage control are again the lower segments.

(no subject)

Date: 22/10/12 18:40 (UTC)(no subject)

Date: 22/10/12 18:43 (UTC)(no subject)

Date: 22/10/12 18:41 (UTC)(no subject)

Date: 22/10/12 18:44 (UTC)I have a problem with this viewpoint. It's not so much that people are living beyond their means; it's that the accepted living standard in the country is beyond the means of a large portion of the country. When paying for food, shelter, and a means of transportation becomes "living beyond your means" then something is wrong. (And I don't mean something fancy, I mean a 1 bedroom apartment for two people, cutting coupons and shopping sales for food, and trying to keep a beater car running. When THAT is "living beyond your means" then something is wrong.)

(no subject)

Date: 22/10/12 19:28 (UTC)How about owning two cars and a 4-bedroom house?

(no subject)

Date: 22/10/12 20:09 (UTC)The fact of the matter is that the anyone not in the upper class in the US (which is generally what you're talking about, although it appears to be the case with other nations as well) has been left behind in the current economy. We pay more and get less. We work harder for lower net salaries. My take-home has diminished each year for the past three, because health insurance and other costs have far outstripped the paltry 2% increases I've been told I should be humbly grateful to receive.

We don't have very many "luxuries" either. No cable, cheap internet, inexpensive phones and phone service. We rarely eat out. Most of the "extras" our kids get are provided by the grandparents, all of whom live on fixed incomes, so you can imagine how little those are.

And I'm doing relatively well. I pay all my bills each month. I even put 10% of my salary into my 401k plan. I have almost nothing left over when it's done, but living pay-check to pay-check is better than consistently falling behind the way some of my friends do when they're forced to choose between medicine and electricity.

You bet I'm living beyond my means, if only just. Living within them means significant detriment to the quality of life of my children and wife.

But please. Judge moar.

(no subject)

Date: 22/10/12 20:15 (UTC)I'm not judging, contrary to how you're trying to frame the conversation.

(no subject)

Date: 22/10/12 20:18 (UTC)(no subject)

Date: 22/10/12 20:25 (UTC)Do you do as you're told you're supposed to?

I get it that the living standard isn't what it used to be. Things have deteriorated from the time of prosperity. But have you thought further back how that came to be? People got crazy on mortgages because they got sucked into the hype of easy loans. There's a proverb, "The one eating the pie isn't the crazy one, the one giving them the pie is the crazy one". Granted. But it's a two-way thing: banks pumping up the property balloon and setting people up in floating sands, and people readily walking into the trap.

I get it that people are having tough times where they shouldn't have. And I wish they didn't. So what can be done? Pay the old loans by taking new ones? Or, maybe, trying to scale back on the expenses? It's a tough decision to do, but is there another option?

(no subject)

Date: 22/10/12 20:35 (UTC)You don't have to have gotten crazy on a mortgage to be in trouble now. Instead of forcing people to leave their homes because their mortgages are under water, we should be arresting bankers, putting them in jail and forcing the rest of them who still get to walk around free to help people refinance to better loan deals.

When the economy tanks, lots of people can no longer live within their means, because their means have suddenly changed significantly. We should be helping these people, not telling them to downsize their lives.

(no subject)

Date: 22/10/12 20:41 (UTC)Emotional hyperbole much?

I asked what can be done. Don't tell me you haven't thought about all these things a lot.

I get it where you're going. The Icelandic model. Default and start anew, scrap the debt and move on as if nothing had happened. Nationalize the banks and use the money to pay for the bad loans and save people who've gone underwater.

Now, do it! We already did.

But you know how we did it? We did arrest bankers and use their money to save people -AND- meanwhile people optimized their expenses. Because the former is only one half of the solution.

I hope next time when a period of prosperity comes, we won't get carried away again like that. Because if we do, it'll mean we're utterly dumb.

(no subject)

Date: 22/10/12 20:48 (UTC)I am stripped back to the bone. A lot of other people are as well. There's almost nothing left to cut.

(no subject)

Date: 22/10/12 20:50 (UTC)Sorry, would've probably been a good joke if we weren't already talking so seriously...

(no subject)

Date: 22/10/12 20:52 (UTC)(no subject)

Date: 22/10/12 20:57 (UTC)(no subject)

Date: 23/10/12 07:30 (UTC)(no subject)

Date: 23/10/12 07:35 (UTC)(no subject)

Date: 23/10/12 10:35 (UTC)(no subject)

Date: 23/10/12 10:48 (UTC)(no subject)

Date: 23/10/12 11:02 (UTC)I see what you mean though, I think there's only like a quarter million Icelanders, I think they're all here.

(no subject)

Date: 22/10/12 20:36 (UTC)(no subject)

Date: 23/10/12 04:08 (UTC)If everyone else jumped off the cliff, would you do it too? That's basically what you're saying, that people can't think for themselves but only listen to what they're told. And it does seem to be the case, but that's not an excuse, it's a problem.

(no subject)

Date: 23/10/12 04:11 (UTC)(no subject)

Date: 24/10/12 23:16 (UTC)300 sq foot for a monthly rent of 1500.00.

The average sized house in the 1950s was about 800 sq. ft, I think.

(no subject)

Date: 23/10/12 04:06 (UTC)(no subject)

Date: 22/10/12 18:45 (UTC)(no subject)

Date: 22/10/12 20:13 (UTC)My favorite observation regarding less equal societies? Big Frickin' Trucks:

Minivans: When you earn enough to not have to worry about being a

dicktough guy.(no subject)

Date: 22/10/12 21:11 (UTC)impliedtossed around here, that nationalizing banks and throwing the bank(st)ers in jail is the end of all problems. I'd just like to ask how we go about it, and where do I subscribe for my free AK47.(no subject)

Date: 22/10/12 21:13 (UTC)(no subject)

Date: 22/10/12 21:14 (UTC)And you now owe me 5 bucks cos that term is trademarked! See? I still have some capitalism in me.

(no subject)

Date: 22/10/12 21:17 (UTC)(no subject)

Date: 22/10/12 21:18 (UTC)Perhaps if we could hand out a few trucks of Molotovs...

(no subject)

Date: 22/10/12 21:20 (UTC)(no subject)

Date: 22/10/12 21:29 (UTC)(no subject)

Date: 23/10/12 04:12 (UTC)(no subject)

Date: 23/10/12 08:23 (UTC)That of course doesn't mean to say anything - as usual.

(no subject)

Date: 23/10/12 20:35 (UTC)What does that have to do with it? I'm not saying that it's unusual for them, I'm saying it's unusual for the common analysis of the topic.

It does mean to say something, I'm sorry if you can't figure out what.

(no subject)

Date: 23/10/12 20:51 (UTC)(no subject)

Date: 23/10/12 23:55 (UTC)(no subject)

Date: 24/10/12 06:06 (UTC)(no subject)

Date: 23/10/12 05:58 (UTC)The US has been running a trade deficit for quite a while, this means other countries, China and the oil rich Arab countries mostly, have been running big surpluses. These have turned into sovereign wealth funds. By running a trade deficit, most of the rich world has thus not only put ourselves in debt but handed a bunch of governments big piles of cash that they need to invest. For the most part, these are the most risk-adverse of investors, meaning they're looking for extremely low risk investments (trivia: stocks are actually not an investment, only investment grade bonds are technically an investment). T-Bills were usually the place where such money would go, and this worked out. The US would be paying out more cash than we bring in, therefore we need to borrow money, the government deficits are part of this cycle and therefore we end up with government debts that pretty much track our trade deficit.

For the past decade, T-Bills paid about nothing however... and they're denominated in USD which have more than lost any of the paltry interest the T-Bills paid anyhow. This left these huge piles of risk adverse foreign money looking for alternatives. AAA bonds of course are a great alternative, as mortgage backed securities have typically been. They paid a bit more and looked very attractive. This caused a huge rush of money, mostly foreign money, to start looking for anything mortgage backed that carried a AAA rating. This was the real source of the investment, not the rich folks in the US but the People's Government in China... a country that saved incredible amounts of money both on an individual and government level, during the early 2000's. This left a bunch of money burning holes in bank's pockets, which in turn made mortgages, and other credit, available to more and more people. This was not driven by inequality in the US but unbalanced trade between the US and other countries. Those who were the investors were actually poorer than most of those doing the borrowing.

Anyhow, those AAA rated bonds turned out not to be so AAA, as only a few people figured out by the end. This was quite different from the crash in 1929.